Today I will launch a quantification team’s official Oil_Hedging two-oil hedging EA. In fact, this hedging strategy is based on the West Texas light crude oil futures in the United States and the North Sea Brent crude oil futures in the United Kingdom. The editor was as early as March. There is a post on the blog, which introduces the regression process and principle in detail from a mathematical point of view.

Today we will formally introduce the principle of this ea from the perspective of financial engineering and how it differs from crude oil hedging on the market.

In financial engineering, it is often not easy to hedge futures contracts, partly for the following reasons:

- The asset that needs to hedge price risk may not be exactly the same as the underlying asset of the futures contract;

- The hedger cannot determine the exact time to buy or sell the asset;

- The hedger may need to liquidate the contract before the futures expires.

The above problems have caused the so-called basis risk. Here we first introduce the concept of “basis”.

Contents of this article

Basis

The usual definition: basis = spot price of the hedged asset-futures price

If the hedged asset is the same as the underlying asset of the futures contract, the basis should be close to zero when the futures expires, and the basis may be positive or negative before the expiry date of the futures contract.

Next, a concept of “cross-hedging” is introduced.

Cross hedge

The assets that the hedger intends to hedge are inconsistent with the underlying assets of the futures contract. In this case, hedging is called cross hedging. In the case of cross-hedging, the basis risk is generally greater. For example, there is an example in financial engineering: For example, an airline needs to hedge against the risks caused by large fluctuations in the price of jet fuel, but there is no futures contract for jet fuel as the basic asset in the market, so it can use civil fuel oil futures contracts. Hedging the price risk of aviation fuel oil. Then another concept is introduced: the “hedging ratio” in cross-hedging.

Hedge ratio

The definition of hedging ratio: the ratio of the number of positions held in the futures contract to the number of risk exposures of the hedged asset. When the two underlying assets that need to be hedged are exactly the same, the hedge ratio is equal to 1. However, in cross-hedging, the hedging ratio used by the hedger should minimize the variance in the value of the entire hedged asset portfolio. The optimal hedge ratio depends on the relationship between the changes in the prices of the two underlying assets to be hedged. Construct a linear regression model.

Δ S = α + h * Δ F + ε

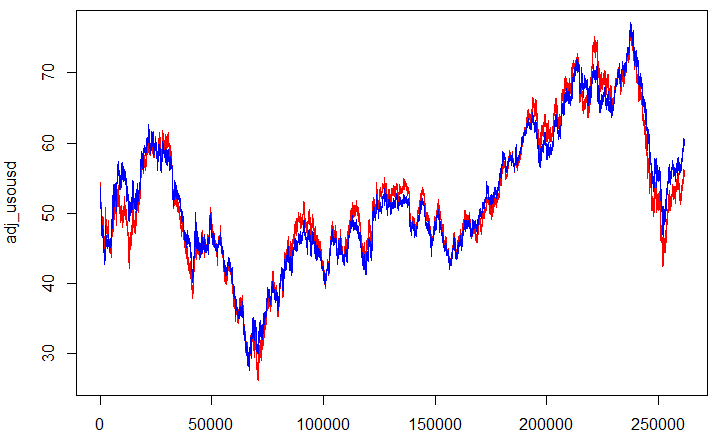

Where α is the intercept term, ε is the residual term, and h* is the slope of the best fitting straight line generated when Δ S is linearly regressed to Δ F, which represents the optimal hedge ratio. Since Δ S and Δ F in the formula are the changes relative to the initial time, the linear regression of the practical absolute price is equivalent to combining the intercepts of the two into α, and the final result is the same. Interested Friends can deduce it by themselves. So I get the following picture in the post

Then we will establish the linear regression model, display it in the price-time coordinate system, and superimpose the real price trend of WTI crude oil to get the following comparison chart.

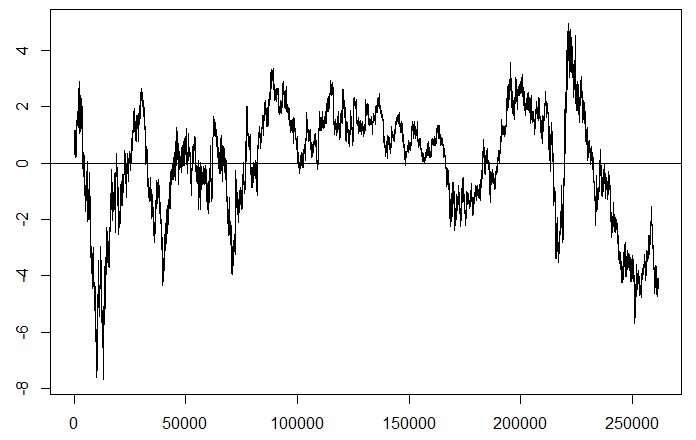

In the figure on the right, it can be seen that the fitting effect of this regression model is still relatively good, then the blue line (the predicted value of U.S. crude oil returned by Brent crude oil) and the red line (the real price of U.S. crude oil) The difference is our profit margin. We make the difference between the two and get the trend chart of the residual term as follows.

Is the arbitrage between the two oil prices on the market reliable?

So what is the difference between the two crude oil futures that we are most exposed to? In fact, they are two futures whose underlying assets are not exactly the same.

Brent crude oil contains four light, sweet crude oils produced in the North Sea Oilfield: Brent, Forties, Ekofisk and Oseberg. Brent crude oil is mined offshore, which is difficult and costly, and is mainly traded in the London commodity futures market.

U.S. WTI crude oil is mainly light crude oil from the Middle East, with low mining difficulty, low cost and good quality. Its delivery point is located in the Cushing area of Oklahoma, USA, and is traded on the New York Mercantile Exchange (NYMEX). US crude oil is a benchmark oil based on futures pricing in the US market, while Brent crude oil is a benchmark oil based on the spot market in the European market.

Therefore, some EAs on the market that claim to be arbitrage between the two oil prices are actually two types of futures with different basic assets from the perspective of financial engineering. If you ignore the hedging ratio, just do the two. The process of converging the oil price difference is actually an incorrect and rigorous approach. We can also see from the price difference chart of the two oils. The price difference between the two oils was pulled to 26.7 US dollars in 2011, and returned to about -1 US dollars in 2016. Such a range and frequency of return are obviously the so-called spread arbitrage on the market. It is unreasonable and not rigorous.

Strategy operation

One. Environmental choice and funding scale

The specific starting capital mainly depends on the broker’s corresponding target contract size, overnight interest and delivery status. Only two platforms, axitrader and gkfx, are recommended here as the recommended operating environment for this strategy. As a neutral technical service provider, other brokers cannot list them one by one. If you are interested, you can also consult customer service in detail.

two. Risk control rules

Risk: The recommended risk control line is 30%.

three. Expected profit

Expected return: 30% nominal retracement rate, actual net worth retracement rate 14.06%, two and a half years compound return of 133.69%, click here to view the detailed backtest report.

four. Disclaimer

As a neutral technical service provider, we only provide technical services. Achievements can only represent the past. Any trading strategy may have certain risks. It is recommended that you carefully consider your risk tolerance.

Этот интересный отчет представляет собой сборник полезных фактов, касающихся актуальных тем. Мы проанализируем данные, чтобы вы могли сделать обоснованные выводы. Читайте, чтобы узнать больше о последних трендах и значимых событиях!

Подробнее можно узнать тут – https://vyvod-iz-zapoya-1.ru/